We’ve just released The Deal, our quarterly review of equity investment in the UK.

Key findings

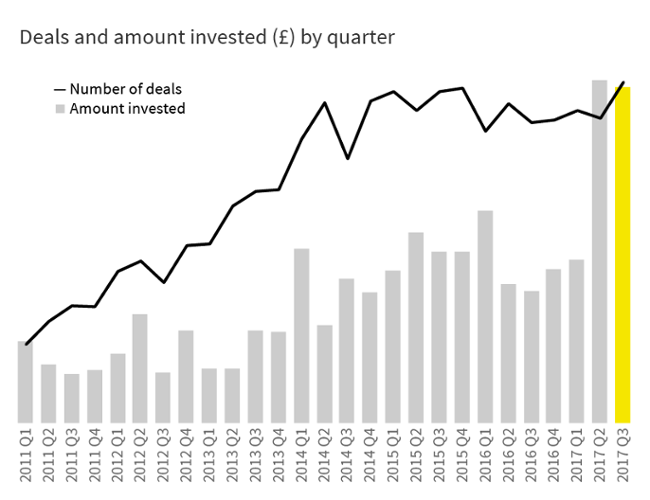

The most deals in a quarter since Beauhurst began tracking the industry in 2011

Continued rise (45%) in the number of investments into growth-stage companies

Record number of “mega-deals” with eight investments of more than £50m

Investment divide between London and other cities growing

Last quarter we saw the amount of investment rocket up to an all-time record, but we were worried that this was a flash in the pan – the chance result of a few mega-deals. This quarter nearly matched that amount of investment and saw a record number of deals, both of which are a cause for celebration.

This growth is mostly due to a rise in investment into growth-stage companies, and especially in mega-deals (£50m+). We view this as a very positive sign that the UK can support the growth of startups beyond the early stage. The long-held view that the UK funding environment does not have the capital to support these deals may no longer apply.

Discover the UK's most innovative companies.

Get access to unrivalled data on all the businesses you need to know about, so you can approach the right leads, at the right time.

Book a 40 minute demo to see all the key features of the Beauhurst platform, plus the depth and breadth of data available.

An associate will work with you to build a sophisticated search, returning a dynamic list of organisations matching your ideal client.