The UK crowd funding landscape in 2019 so far

|

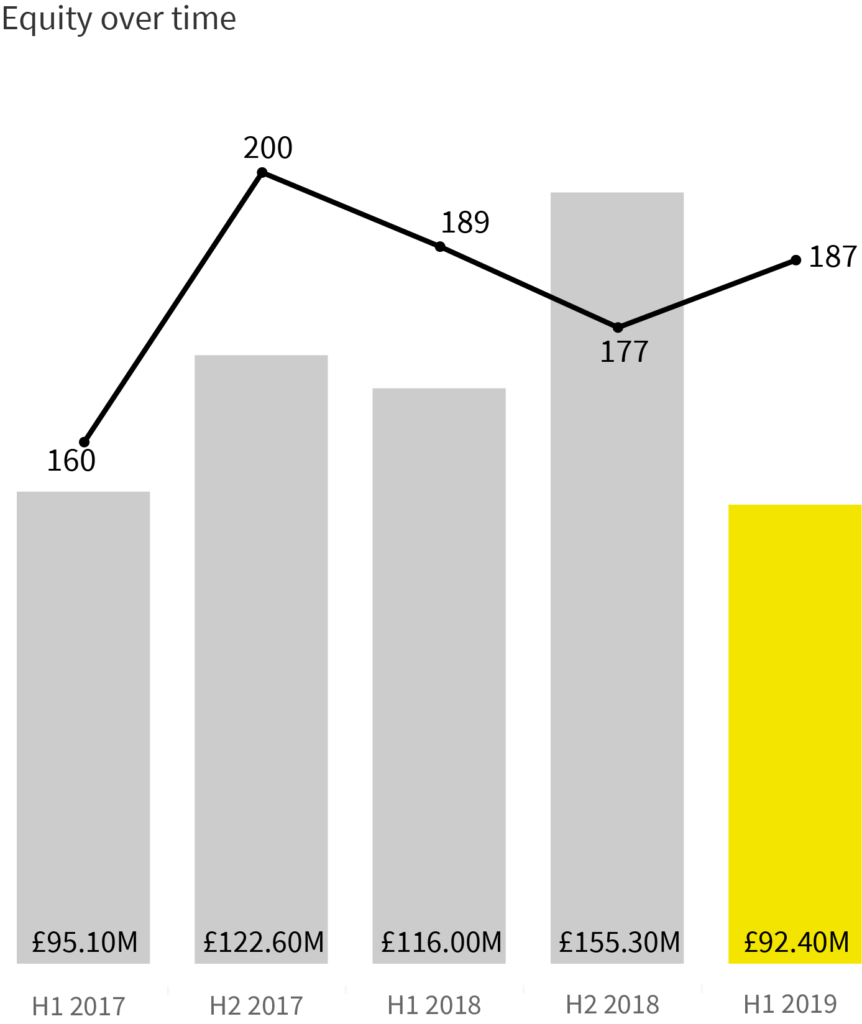

‘The amount invested in to companies through crowdfunding platforms has returned to levels seen in H1 2017. Deal numbers may be stabilising, having bumped between 160 and 200 deals for each of the last five halves.'

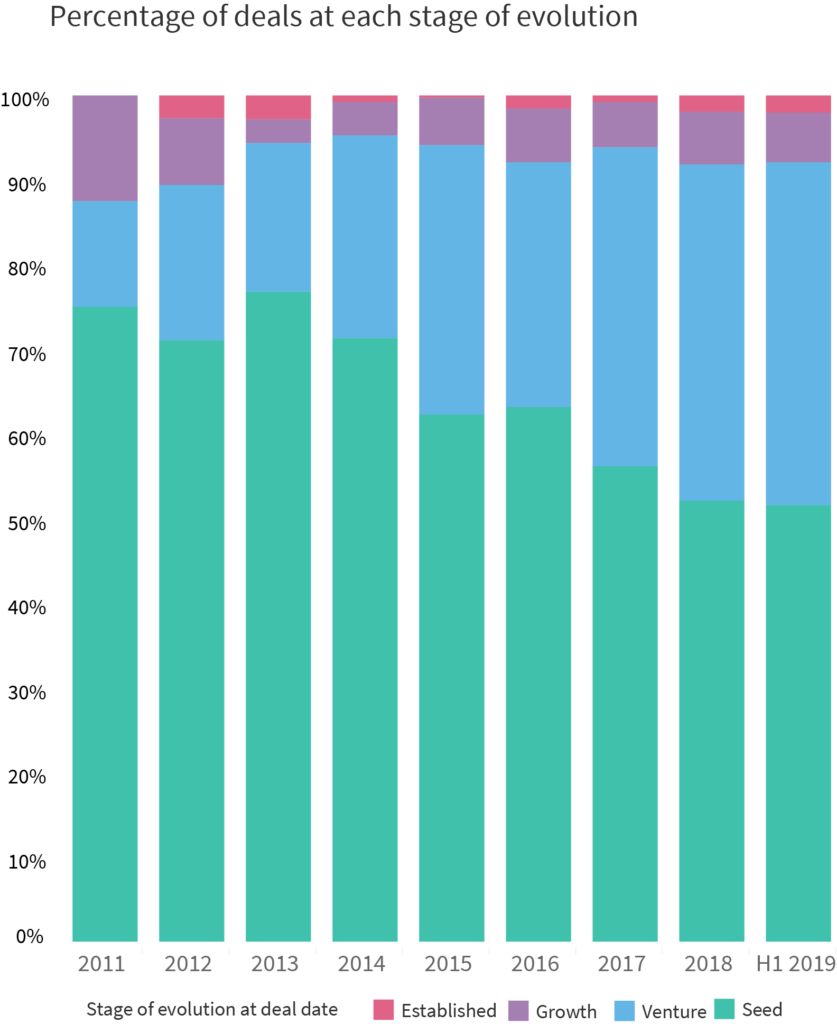

‘It is interesting to see that, despite its digital and arguably delocalised model of investment, crowdfunding is still investing largely in London-based entrepreneurs and their ideas, despite only representing 37% of the UK’s active ambitious companies.’