The latest data on equity investment trends in the UK. We’ve analysed every publicly-announced equity fundraising in H1 2019, to spot emerging trends and patterns in the market.

See our yearly edition, The Deal, for in-depth analysis and features on key market trends.

Key findings

Number of deals

1

Amount invested

£B

Difference from H2 2018

+%

Difference from H2 2018

+%

H1 2019 was the best first half on record, with a 15% increase in the total amount of investment received by the UK’s startups and scaleups.

The number of deals rose 10% since the previous half, and the majority of the increase was at the seed-stage.

There was also a 17% increase in the number of growth stage deals and their average size rose from £16m to £17m.

FinTech saw more money invested than in any other half, and has already beaten figures for the whole of 2018. AI was the only sector to achieve a record number of deals.

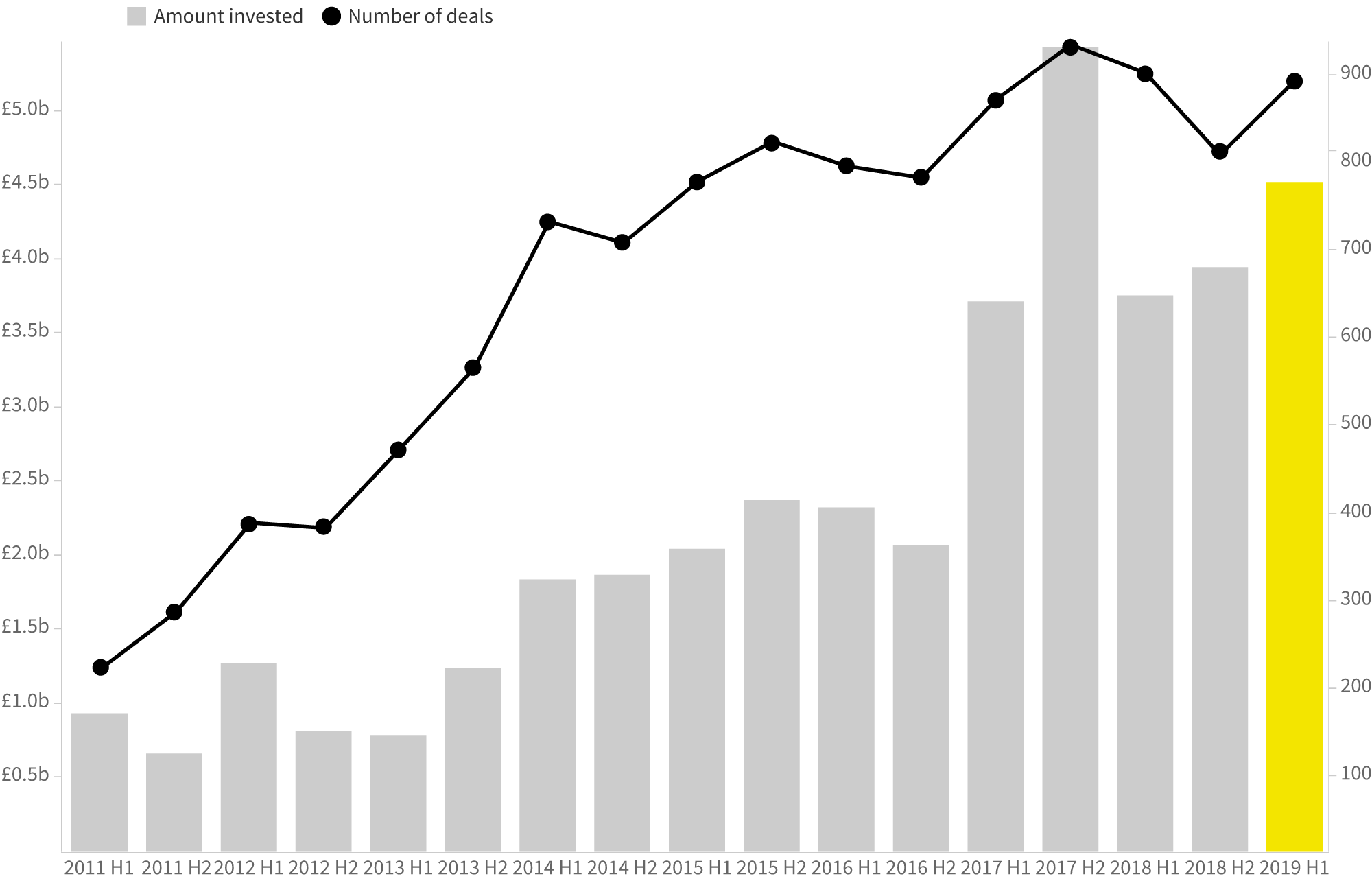

deal numbers and amount invested

Hot on the tails of investment records set in H2 2017, this half has been the second best on record. Already securing a higher amount than in the whole of 2016, this year is now on track to be a record year of funding, surpassing the peak seen in 2017.

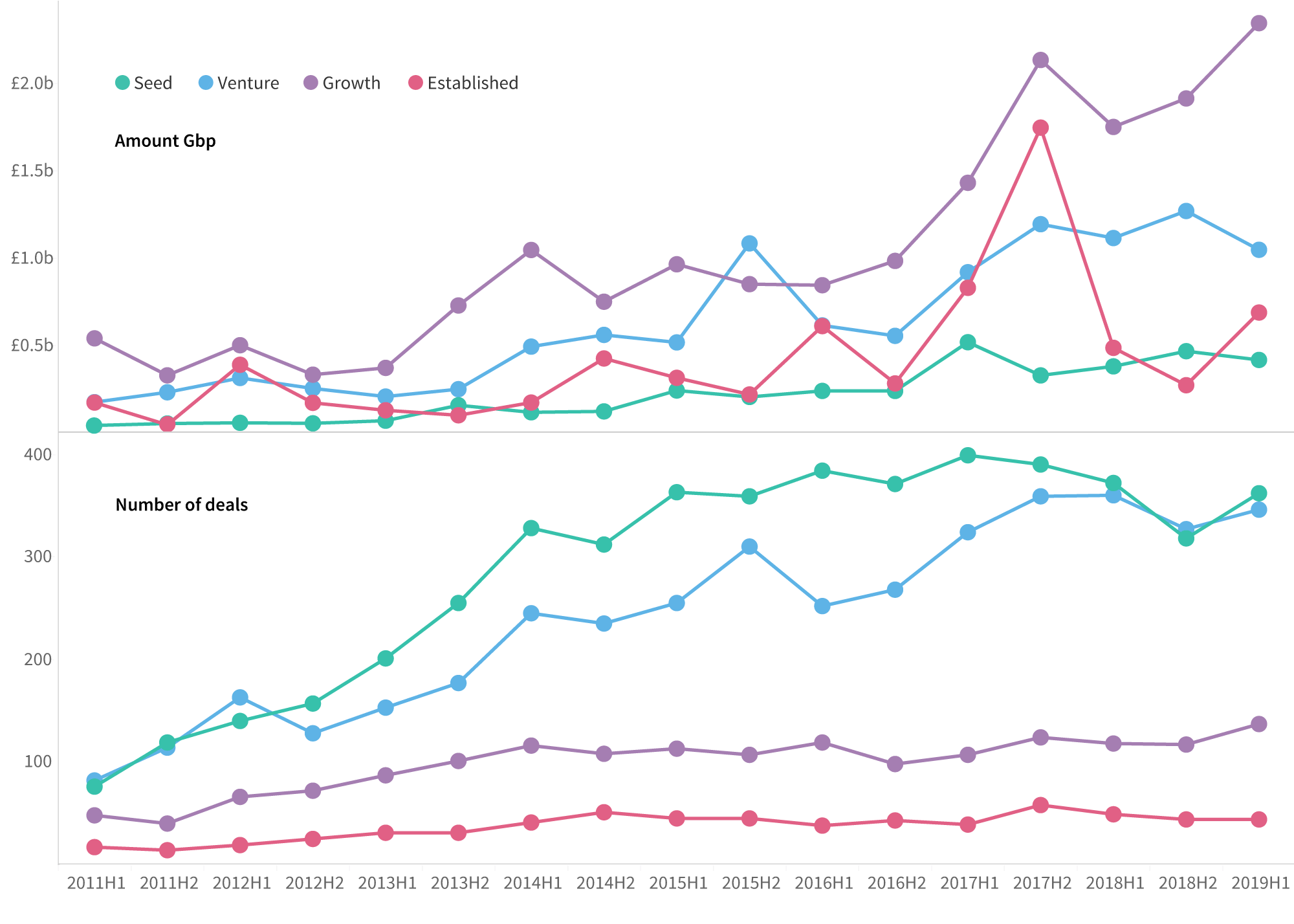

Investment stages

Deal numbers at the growth stage reached an all time high, with 137 investments made over the half. The value of these investments rocketed, with £2.4b invested into growth stage companies. Inside of this category, the number of megadeals has been consistently high since 2017, making them a permanent feature of the funding landscape.

The number of deals at the seed stage grew by 14%, the first increase since H1 2017. This rise is a good sign of recovery for early stage investments following a slump in 2018.

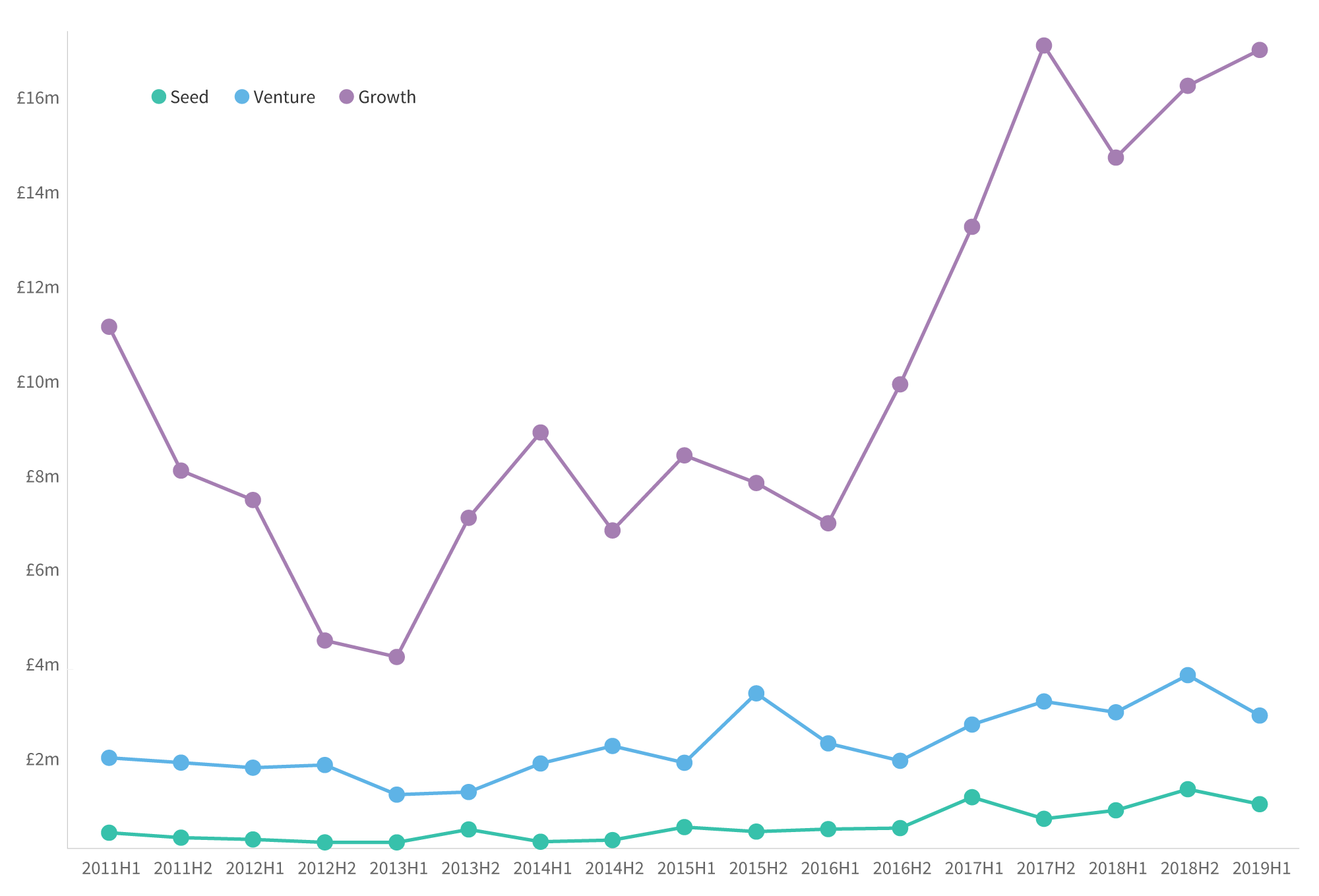

deal numbers and amount invested by company stage

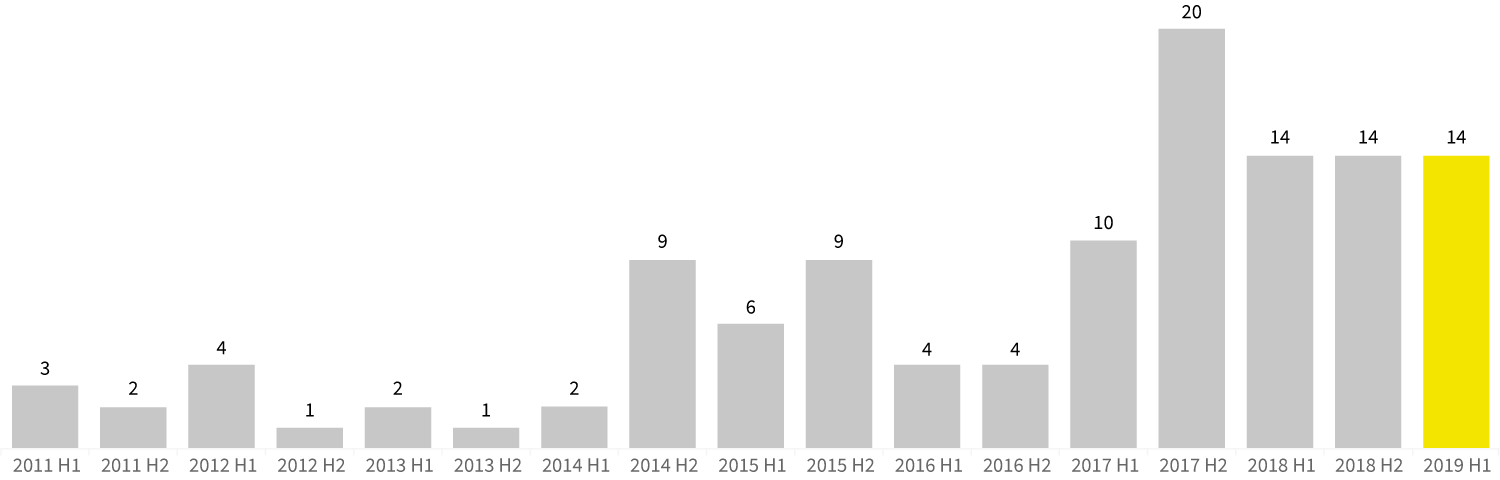

number of megadeals (£50m+)

After a troubling few years for seed stage deals, it’s a relief to see some pick up in the number of investments being made. We're not completely in the clear yet – levels have yet to return to those seen in 2018 H1 – but seed stage deals are finally roaming north of venture stage numbers, something we hope to see continue in the future.

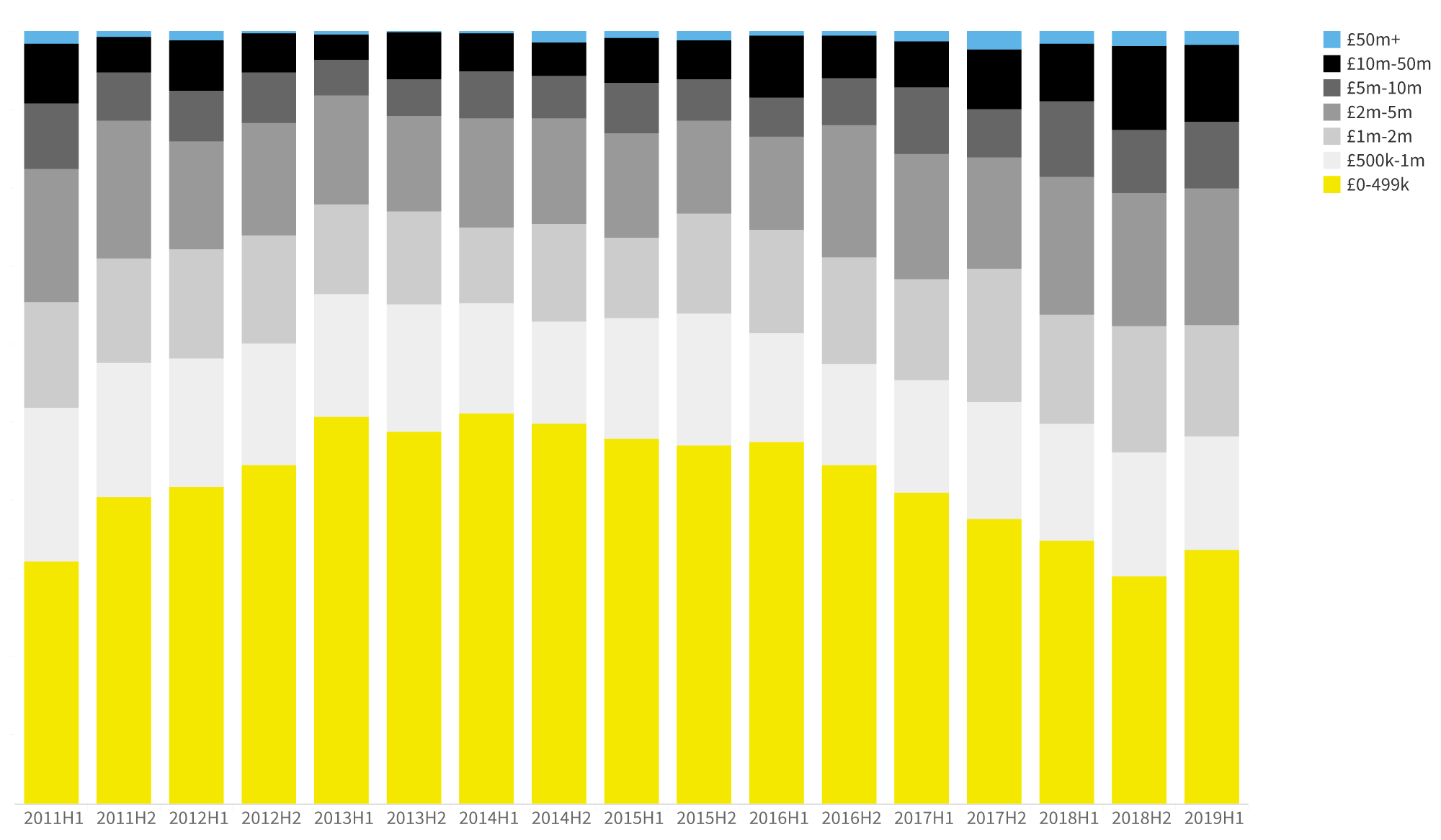

Investment sizes

After several years of a slow and steady decline in the proportion of deals below £500k, the first half of 2019 saw a small rise, which is good news for small businesses. The proportion of deals made at the opposite end of the spectrum also increased, squeezing the proportion of deals at the £500k – £2m mark.

In addition, the average size of growth stage deals has continued to climb, whilst seed and venture deals slightly dropped during the half. Does this growing imbalance mean fast growing businesses will have less chance of success surviving the yawning chasm between funding rounds?

* This data excludes Deliveroo’s $575m raise led by Amazon in May 2019, as the deal has been paused for investigation by the Competition and Markets Authority (CMA).

deal sizes, percent share per Half

average deal sizes per half, by stage of evolution

Over the last 5 years the average size of growth stage deals has increased two fold; this is a product of the rise of megadeals and mega funds. It remains to be seen what the impact of this will be on the high-growth ecosystem; do fewer but bigger deals mean that some companies are missing out on funding, or does the need to raise finance less frequently in fact make life easier for ambitious businesses? Whatever the case, different companies have different needs, so we suspect that more diversity in deal sizes can only be a good thing.

Sector focus

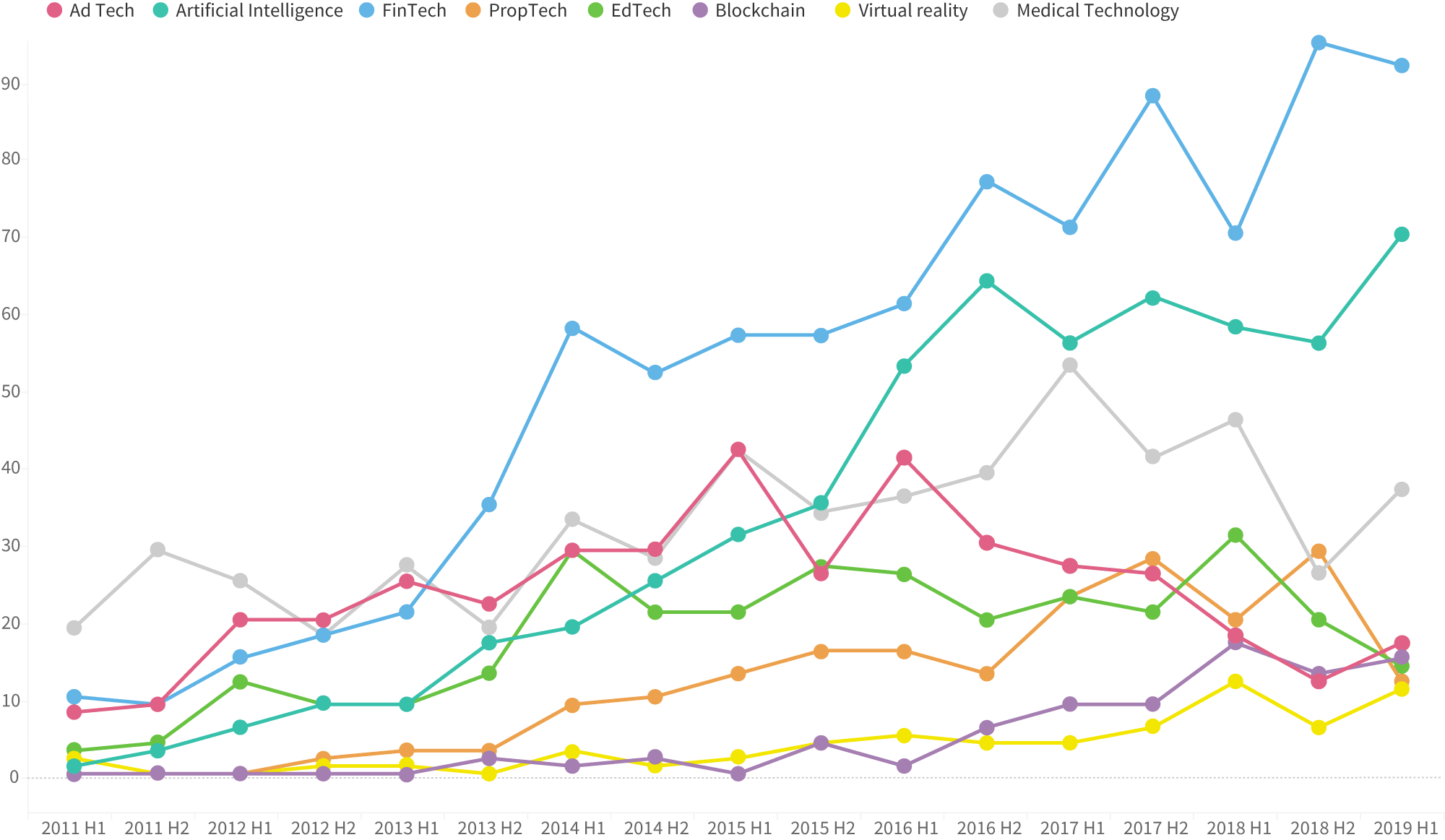

This half was especially good for Artificial Intelligence, the only sector that has achieved a record number of deals, with 70 investments made. Despite this, the amount invested into AI companies was £355m, failing to reach the £439m record set in the previous half.

Many others sectors performed better than the previous half, including MedTech, VR and Blockchain. AdTech saw a 14% rise in deal numbers, the first increase since H1 2016.

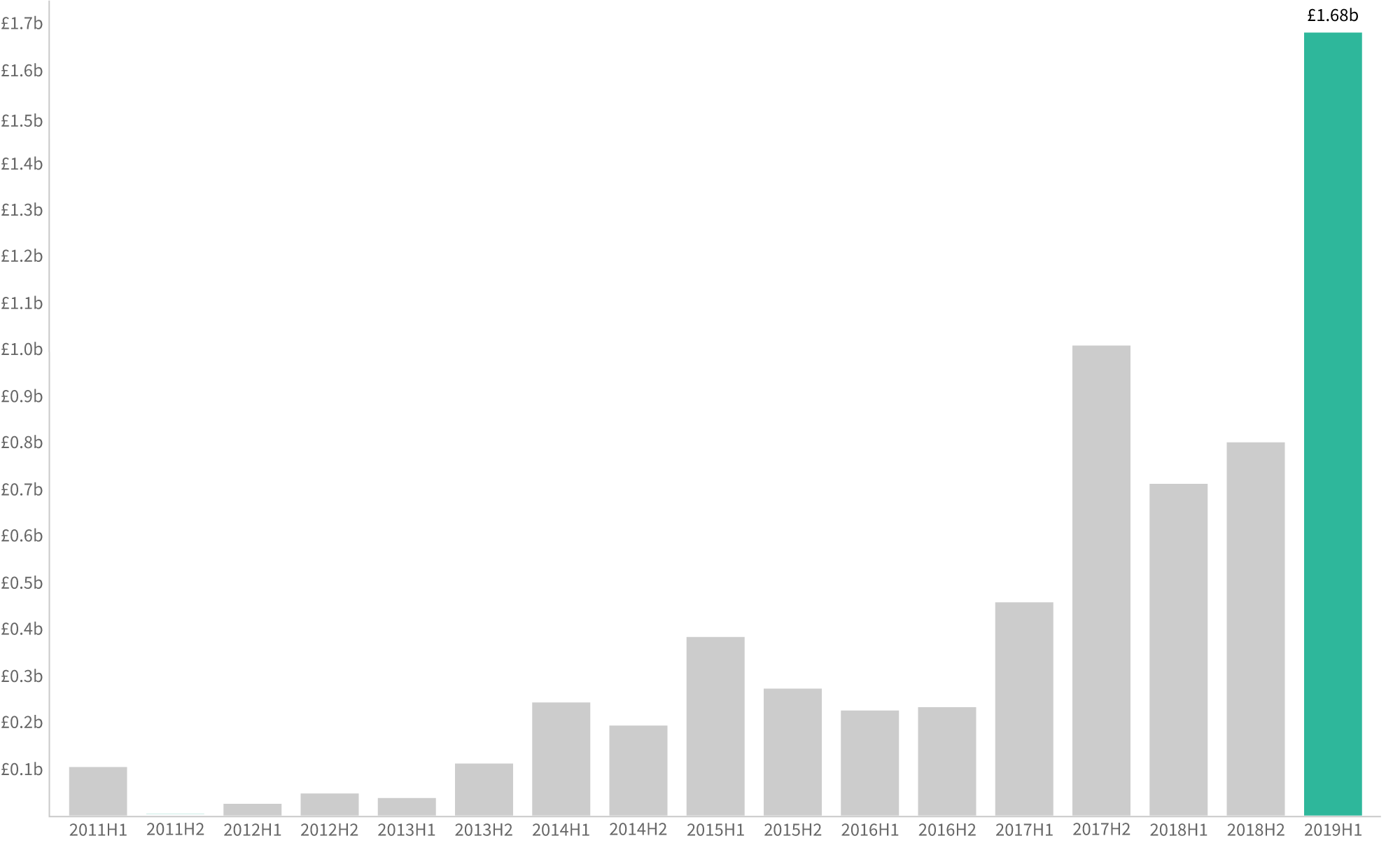

Although FinTech suffered a fall in deal numbers, it has had a tremendous half for pounds invested. £1.7b has been channeled into the sector, surpassing the amount met in 2018 as a whole. In the UK’s high-growth scene, FinTech remains king.

Deal numbers, selected sectors

Amount invested, fintech

The biggest deals of the half

Oaknorth Bank

£440m

Ovo Energy

£200m

Checkout.com

£176m

iwoca

£150m

WorldRemit

£138m

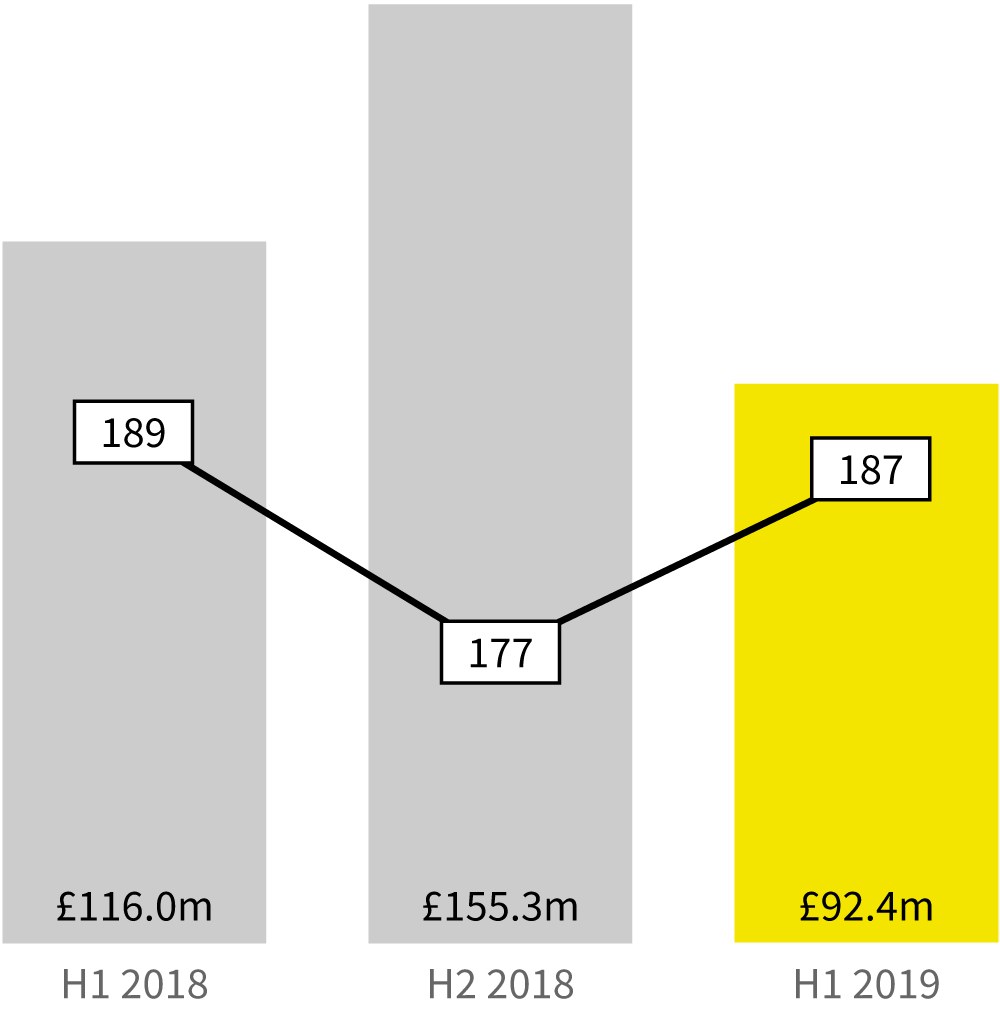

Crowdfunding in H1 2019

British crowdfunders invested £92.4m through 187 deals in the first half of 2019.

The amount invested in to companies through crowdfunding platforms has returned to levels seen in H1 2017. It appears as if deal numbers are also starting to flatline, having bumped between 160 and 200 deals completed for each of the last five halves. Is this rate the new normal for crowd funder’s share of the equity market?

major crowdfunding platforms, deals

seedrs

98 (incl. 28 pre-emptions)

crowdcube

83 (incl. 3 pre-emptions)

Crowdfunding investments

Crowdcube

£55.6m 83 deals

Seedrs

£36.8m 98 deals

Have you seen our full year report?

The Deal is our free, detailed analysis of every equity fundraising in 2018. We look at the stories behind the deals, and examine which companies, investors and sectors are making waves.