The latest data on equity investment trends in the UK. We’ve analysed every publicly-announced equity fundraising in Q3 2018, to spot emerging trends and patterns in the market.

See our yearly edition, The Deal, for in-depth analysis and features on key market trends.

Key findings

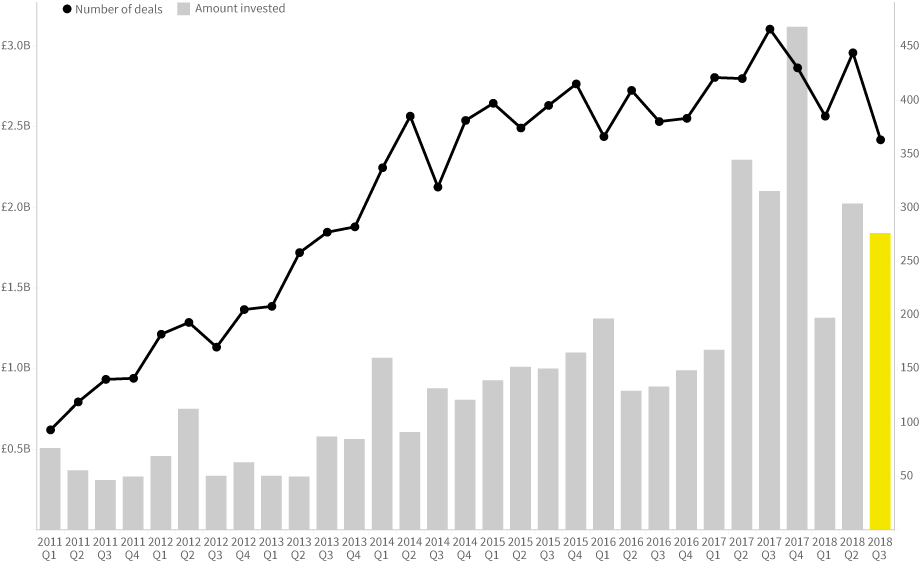

Number of deals

Amount invested

£B

Difference from Q2 2018

-%

Difference from q2 2018

-%

Deal numbers fell by 18% from the previous quarter, making this the lowest quarter for deals since Q3 2014.

The amount invested remained high. Despite falling 9% from the previous quarter, Q3 2018 was the fifth highest quarter on record.

Growth in the Fintech sector continued, despite increasing uncertainty around the terms of Brexit.

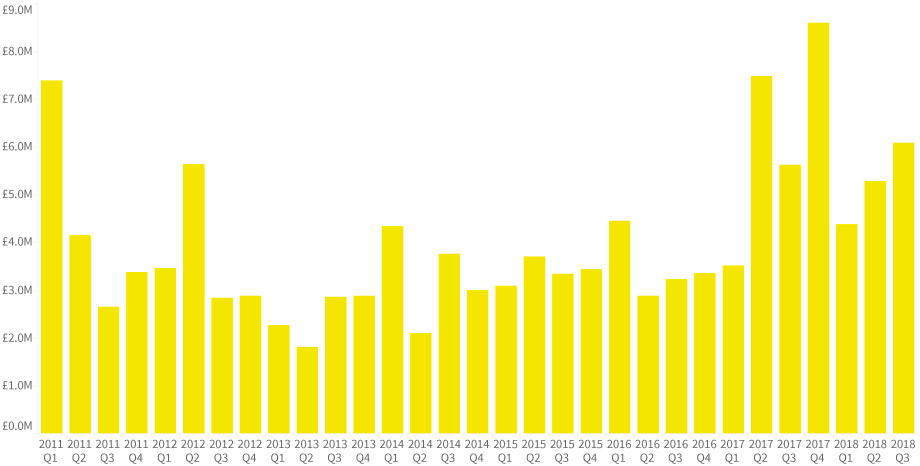

The average deal size increased 15% from last quarter to £6.1m, and has almost doubled since the same quarter two years ago.

deal numbers and amount invested

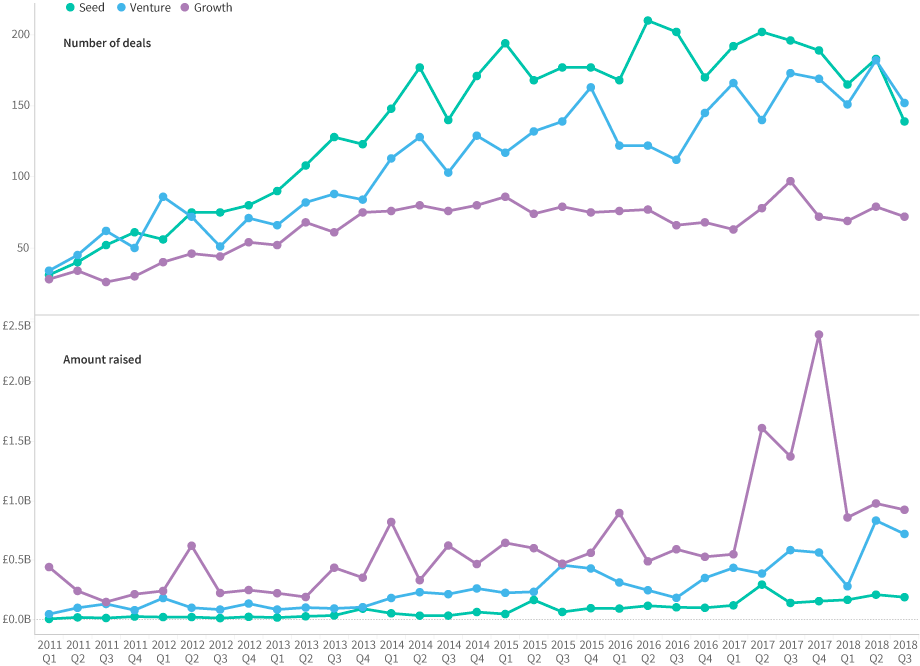

Investment stages

Deal numbers fell at every stage of company evolution, but most sharply for seed investments, where they reached their lowest since Q4 2013. The amount invested remained fairly level at this stage, suggesting more money going into fewer deals. Indeed, the average deal size has risen 15% from last quarter to £6.1m, and almost doubled since Q3 2016. The number of seed-stage deals also fell below venture-stage deals for the first time since 2012. We think investors are looking for safer bets in the current climate.

The huge amounts invested at the growth stage last year have fallen back to more normal levels, but are still higher than we were seeing pre-2017 spike.

deal numbers and amount invested by company stage

average deal size over time

[INSERT_ELEMENTOR id="6554"]

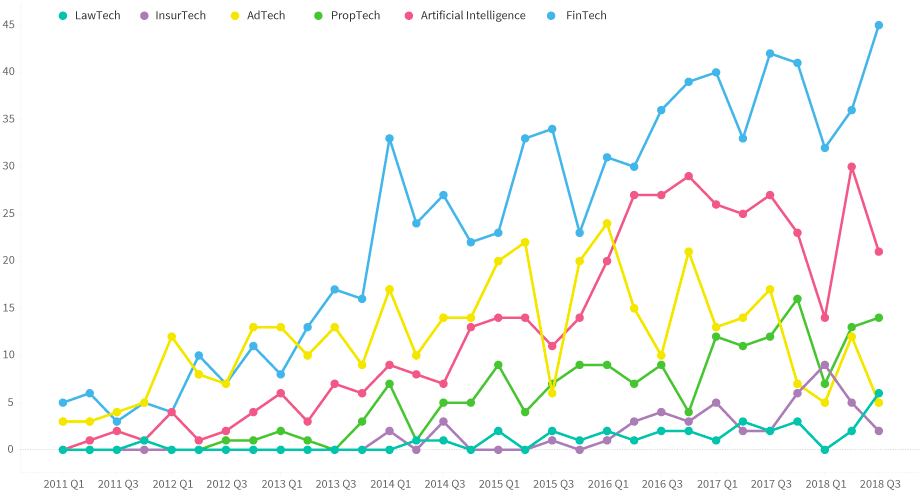

Sector focus

While the quarter was generally poor for deal numbers, Fintech saw the highest number of deals on record, and £309m invested into the sector. Investor appetite for the vertical has shown no signs of slowing down despite increasing Brexit uncertainty — we can only hope the supply of talent manages to keep up.

Investment into Adtech continued to decline from its peak in 2016, with numbers falling below both Lawtech and Proptech for the first time. We think these two sectors are on the up and ones to watch.

Deal numbers, selected sectors

The biggest deals of the quarter

greensill

£189m

orchard therapeutics

£118m

OakNorth Bank

£77m

Artios Pharma

£66m

Secret Escapes

£52m

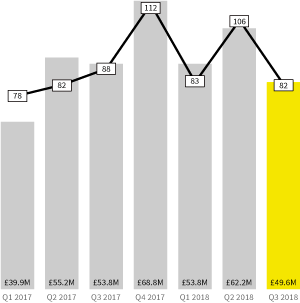

Crowdfunding in Q3 2018

British crowdfunders invested £49.6m in the third quarter of 2018, over 82 deals. This total round amount (including participations from other investor types) of these deals was £65.3m.

major crowdfunding platforms, deals

crowdcube

42 (incl. 2 pre-emptions)

seedrs

31 (incl. 6 pre-emptions, 1 convertible campaign)

syndicateroom

6

Crowdfunding investments

Crowdcube £27.4m 42 deals

Seedrs £13.3m 31 deals

SyndicateRoom £4.5m 6 deals

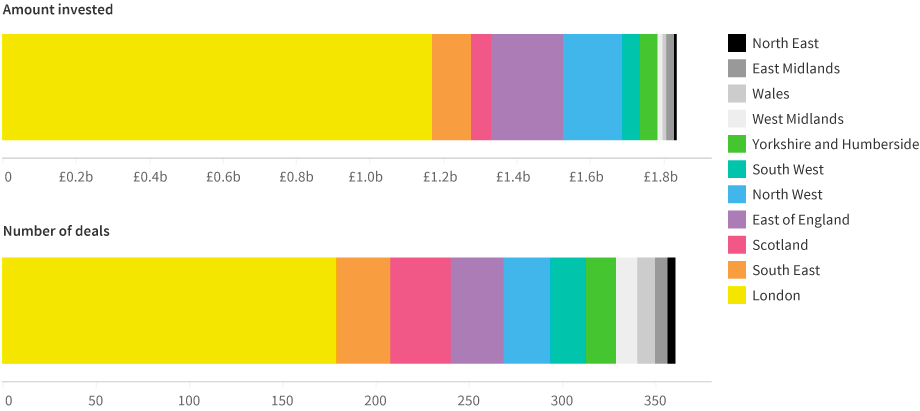

Regional distribution

Dominating as usual, London took the lions share of the amount invested, accounting for 64%. For number of deals, this figure was 50%. The South East and Scotland had fairly strong quarters, accounting for 8 and 9% respectively.

regional share of h1 2018 deals

Have you seen our full year report?

The Deal is our free, detailed analysis of every equity fundraising in 2017. We look at the stories behind the deals, and examine which companies, investors and sectors are making waves.