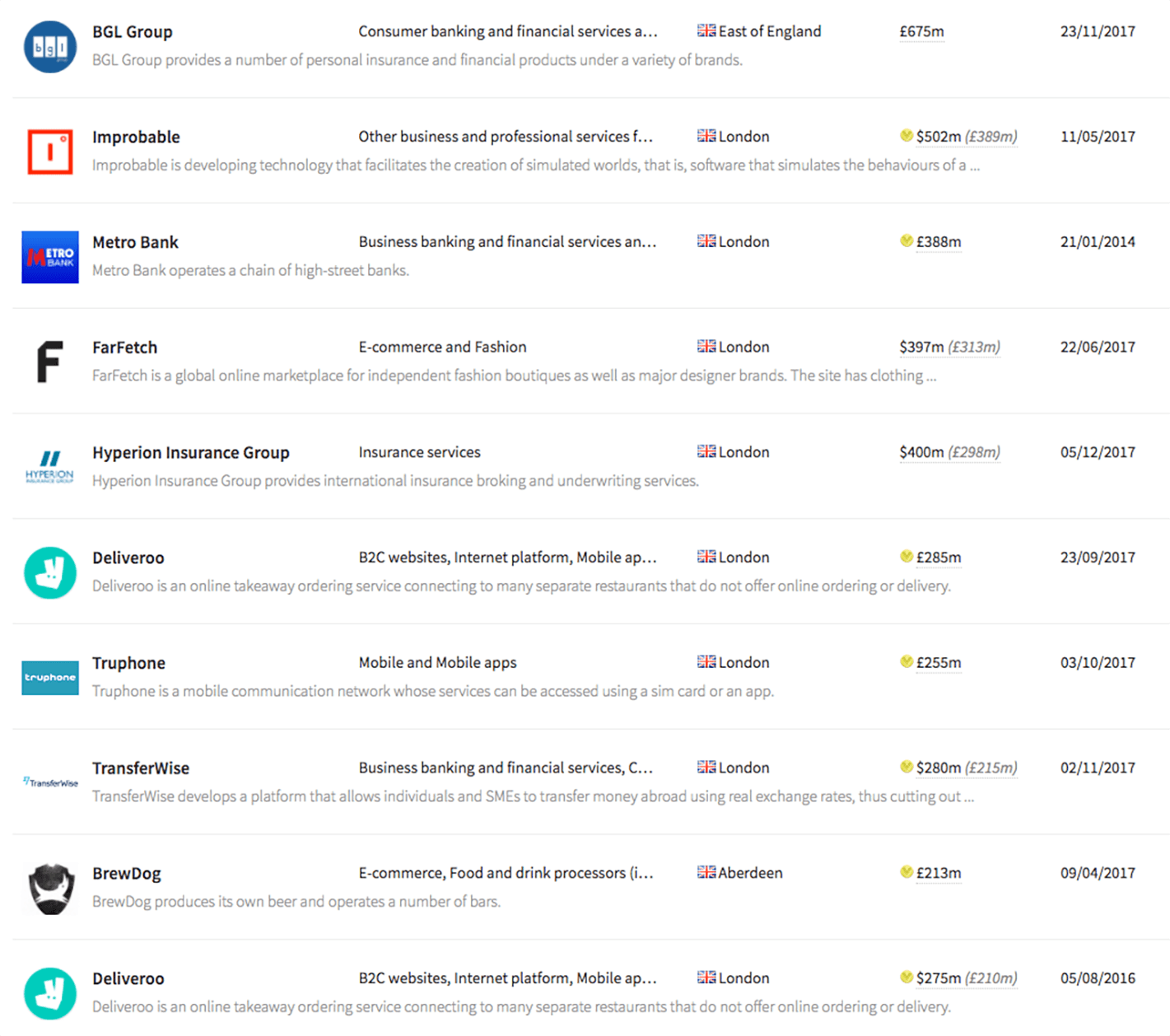

Lots of ambitious companies use external finance to fuel their growth; this can be in the form of debt, private market equity investment and public market equity. Given the rapidly increasing volume of megadeals being completed by the private market that we’ve documented elsewhere, we’ve taken a look below at the relationship between private equity raising and raises on the LSE’s junior market AIM, which is usually the first public port of call for young companies.

PRIVATE VS PUBLIC MARKETS

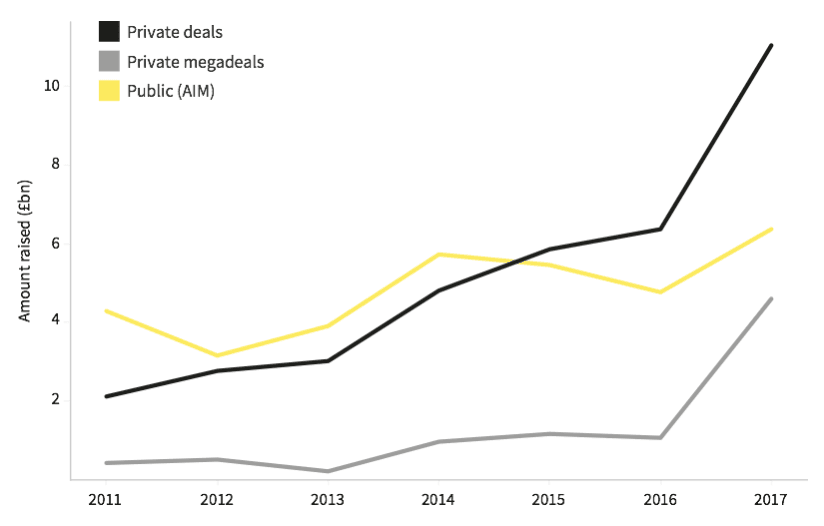

In 2015 the annual amount raised by companies in private deals overtook the amount raised on the public markets via AIM. Since then this gap in value has been growing, with the most recent figures from 2017 showing that 73% more (£4.67bn) was raised privately than through new and further listings on AIM. These figures hint at a number of changes within the private funding landscape over the past few years.