At Beauhurst, we’ve a created a unique and comprehensive database of the UK’s private businesses. While many of these companies will go on to be worth many millions, it can be very difficult to value them early on in their growth. Using previous valuations and comparables, our platform helps finance professionals to value young companies. So how exactly do you value a startup?

Forward-looking valuations

Many metrics can be used. Sometimes, the valuation of a company will focus on how much profit the business currently generates. In this case the value could reach up to seven or eight multiples of how much profit they’re currently making per year. However, this becomes problematic for startups, the vast majority of which fail to generate profit during a significant part of their initial lifecycle. Furthermore, after many years of unprofitability, successful startups can then become very profitable indeed (Facebook took five years to turn a profit). Valuations with younger companies are very often extremely forward looking, with emphasis put on growth and revenue/profit potential rather than current status.

How does Beauhurst help?

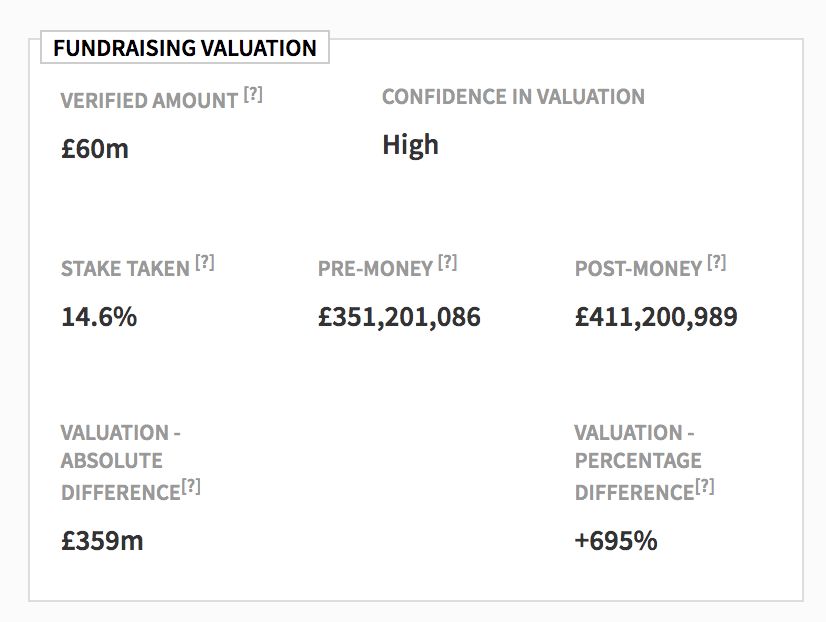

It’s possible to discover a startup’s valuation at the point of equity investment through company filings – even when not announced to the press. Companies are obliged to disclose whenever they issue a new round of shares, and at what price the new shares have been bought. This means a total share value can be calculated. Because this isn’t always as straightforward as it might seem, we even provide a confidence measure, showing where we think that figures might need to be taken with a pinch of salt, and where they should be reasonably reliable.